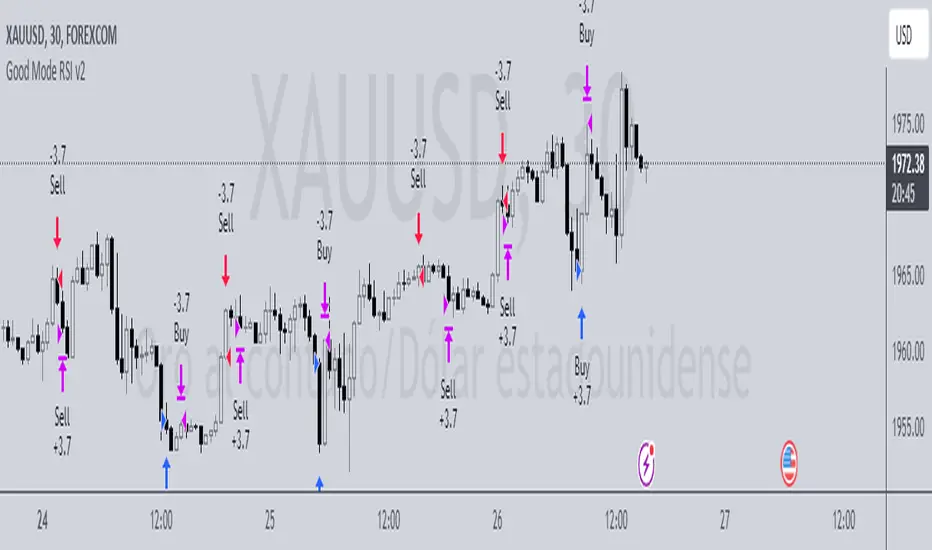

Baseline Cross Qualifier Volatility Strategy with HMA Trend BiasFor trading ES on 30min Chart

Trading Rules

Post Baseline Cross Qualifier (PBCQ): If price crosses the baseline but the trade is invalid due to additional qualifiers, then the strategy doesn't enter a trade on that candle. This setting allows you override this disqualification in the following manner: If price crosses XX bars ago and is now qualified by other qualifiers, then the strategy enters a trade.

Volatility: If price crosses the baseline, we check to see how far it has moved in terms of multiples of volatility denoted in price (ATR x multiple). If price has moved by at least "Qualifier multiplier" and less than "Range Multiplier", then the strategy enters a trade. This range is shown on the chart with yellow area that tracks price above/blow the baseline. Also, see the dots at the top of the chart. If the dots are green, then price passes the volatility test for a long. If the dots are red, then price passes the volatility test for a short.

Take Profit/Stoploss Quantity Removed

1 Take Profit: 100% of the trade is closed when the profit target or stoploss is reached.

2 Take Profits: Quantity is split 50/50 between Take Profit 1 and Take Profit 2

3 Take Profits: Quantify is split 50/25/25.

Stratgey Inputs

Baseline Length

37

Post Baseline Cross Qualifier Enabled

On

Post Baseline Cross Qualifier Bars Ago

9

ATR Length

9

Volatility Multiplier

0

Volatility Range Multiplier

10

Volatility Qualifier Multiplier

2

Take Profit Type

1 Take Profit

HMA Length

11

ابحث في النصوص البرمجية عن "take profit"

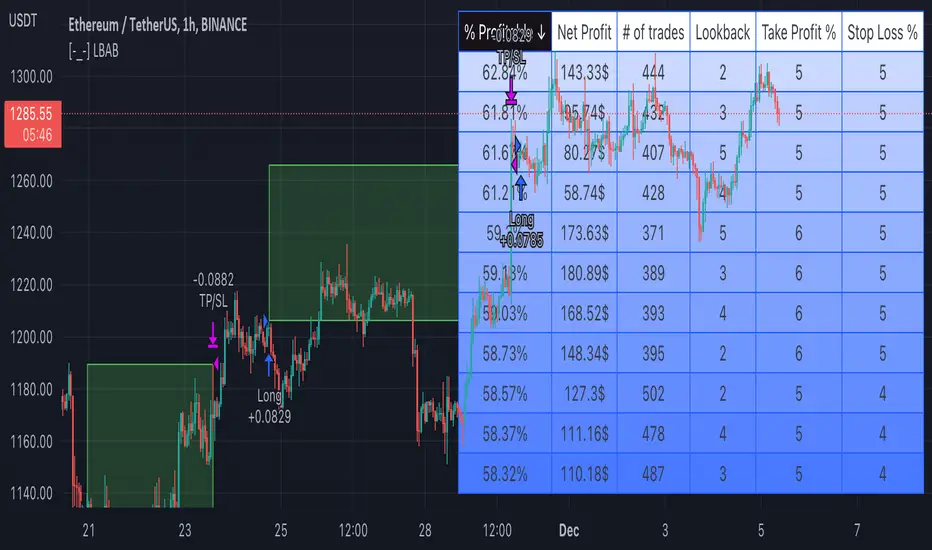

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

[MT] Strategy Backtest Template| Initial Release | | EN |

An update of my old script, this script is designed so that it can be used as a template for all those traders who want to save time when programming their strategy and backtesting it, having functions already programmed that in normal development would take you more time to program, with this template you can simply add your favorite indicator and thus be able to take advantage of all the functions that this template has.

🔴Stop Loss and 🟢Take Profit:

No need to mention that it is a Stop Loss and a Take Profit, within these functions we find the options of: fixed percentage (%), fixed price ($), ATR, especially for Stop Loss we find the Pivot Points, in addition to this, the price range between the entry and the Stop Loss can be converted into a trailing stop loss, instead, especially for the Take Profit we have an option to choose a 1:X ratio that complements very well with the Pivot Points.

📈Heikin Ashi Based Entries:

Heikin Ashi entries are trades that are calculated based on Heikin Ashi candles but their price is executed to Japanese candles, thus avoiding false results that occur in Heikin candlestick charts, this making in certain cases better results in strategies that are executed with this option compared to Japanese candlesticks.

📊Dashboard:

A more visual and organized way to see the results and necessary data produced by our strategy, among them we can see the dates between which our operations are made regardless if you have activated some time filter, usual data such as Profit, Win Rate, Profit factor are also displayed in this panel, additionally data such as the total number of operations, how many were gains and how many losses, the average profit and loss for each operation and finally the maximum profits and losses followed, which are data that will be very useful to us when we elaborate our strategies.

Feel free to use this template to program your own strategies, if you find errors or want to request a new feature let me know in the comments or through my social networks found in my tradingview profile.

| Update 1.1 | | EN |

➕Additions: '

Time sessions filter and days of the week filter added to the time filter section.

Option to add leverage to the strategy.

5 Moving Averages, RSI, Stochastic RSI, ADX, and Parabolic Sar have been added as indicators for the strategy.

You can choose from the 6 available indicators the way to trade, entry alert or entry filter.

Added the option of ATR for Take Profit.

Ticker information and timeframe are now displayed on the dashboard.

Added display customization and color customization of indicator plots.

Added customization of display and color plots of trades displayed on chart.

📝Changes:

Now when activating the time filter it is optional to add a start or end date and time, being able to only add a start date or only an end date.

Operation plots have been changed from plot() to line creation with line.new().

Indicator plots can now be controlled from the "plots" section.

Acceptable and deniable range of profit, winrate and profit factor can now be chosen from the "plots" section to be displayed on the dashboard.

Aesthetic changes in the section separations within the settings section and within the code itself.

The function that made the indicators give inputs based on heikin ashi candles has been changed, see the code for more information.

⚙️Fixes:

Dashboard label now projects correctly on all timeframes including custom timeframes.

Removed unnecessary lines and variables to take up less code space.

All code in general has been optimized to avoid the use of variables, unnecessary lines and avoid unnecessary calculations, freeing up space to declare more variables and be able to use fewer lines of code.

| Lanzamiento Inicial | | ES |

Una actualización de mi antiguo script, este script está diseñado para que pueda ser usado como una plantilla para todos aquellos traders que quieran ahorrar tiempo al programar su estrategia y hacer un backtesting de ella, teniendo funciones ya programadas que en el desarrollo normal te tomaría más tiempo programar, con esta plantilla puedes simplemente agregar tu indicador favorito y así poder aprovechar todas las funciones que tiene esta plantilla.

🔴Stop Loss y 🟢Take Profit:

No hace falta mencionar que es un Stop Loss y un Take Profit, dentro de estas funciones encontramos las opciones de: porcentaje fijo (%), precio fijo ($), ATR, en especial para Stop Loss encontramos los Pivot Points, adicionalmente a esto, el rango de precio entre la entrada y el Stop Loss se puede convertir en un trailing stop loss, en cambio, especialmente para el Take Profit tenemos una opción para elegir un ratio 1:X que se complementa muy bien con los Pivot Points.

📈Entradas Basadas en Heikin Ashi:

Las entradas Heikin Ashi son operaciones que son calculados en base a las velas Heikin Ashi pero su precio esta ejecutado a velas japonesas, evitando así́ los falsos resultados que se producen en graficas de velas Heikin, esto haciendo que en ciertos casos se obtengan mejores resultados en las estrategias que son ejecutadas con esta opción en comparación con las velas japonesas.

📊Panel de Control:

Una manera más visual y organizada de ver los resultados y datos necesarios producidos por nuestra estrategia, entre ellos podemos ver las fechas entre las que se hacen nuestras operaciones independientemente si se tiene activado algún filtro de tiempo, datos usuales como el Profit, Win Rate, Profit factor también son mostrados en este panel, adicionalmente se agregaron datos como el número total de operaciones, cuantos fueron ganancias y cuantos perdidas, el promedio de ganancias y pérdidas por cada operación y por ultimo las máximas ganancias y pérdidas seguidas, que son datos que nos serán muy útiles al elaborar nuestras estrategias.

Siéntete libre de usar esta plantilla para programar tus propias estrategias, si encuentras errores o quieres solicitar una nueva función házmelo saber en los comentarios o a través de mis redes sociales que se encuentran en mi perfil de tradingview.

| Actualización 1.1 | | ES |

➕Añadidos:

Filtro de sesiones de tiempo y filtro de días de la semana agregados al apartado de filtro de tiempo.

Opción para agregar apalancamiento a la estrategia.

5 Moving Averages, RSI, Stochastic RSI, ADX, y Parabolic Sar se han agregado como indicadores para la estrategia.

Puedes escoger entre los 6 indicadores disponibles la forma de operar, alerta de entrada o filtro de entrada.

Añadido la opción de ATR para Take Profit.

La información del ticker y la temporalidad ahora se muestran en el dashboard.

Añadido personalización de visualización y color de los plots de indicadores.

Añadido personalización de visualización y color de los plots de operaciones mostradas en grafica.

📝Cambios:

Ahora al activar el filtro de tiempo es opcional añadir una fecha y hora de inicio o fin, pudiendo únicamente agregar una fecha de inicio o solamente una fecha de fin.

Los plots de operaciones han cambiados de plot() a creación de líneas con line.new().

Los plots de indicadores ahora se pueden controlar desde el apartado "plots".

Ahora se puede elegir el rango aceptable y negable de profit, winrate y profit factor desde el apartado "plots" para mostrarse en el dashboard.

Cambios estéticos en las separaciones de secciones dentro del apartado de configuraciones y dentro del propio código.

Se ha cambiado la función que hacía que los indicadores dieran entradas en base a velas heikin ashi, mire el código para más información.

⚙️Arreglos:

El dashboard label ahora se proyecta correctamente en todas las temporalidades incluyendo las temporalidades personalizadas.

Se han eliminado líneas y variables innecesarias para ocupar menos espacio en el código.

Se ha optimizado todo el código en general para evitar el uso de variables, líneas innecesarias y evitar los cálculos innecesarios, liberando espacio para declarar más variables y poder utilizar menos líneas de código.

Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2

This script was originally shared by Wunderbit as a free open source script for the community to work with. This is my second published iteration of this idea.

WHAT THIS SCRIPT DOES:

It is intended for use on an algorithmic bot trading platform but can be used for scalping and manual trading.

This strategy is based on the trend-following momentum indicator . It includes the Money Flow index as an additional point for entry.

This is a new and improved version geared for lower timeframes (15-5 minutes), but can be run on larger ones as well. I am testing it live as my high frequency trader.

HOW IT DOES IT:

It uses a combination of MACD and MFI indicators to create entry signals. Parameters for each indicator have been surfaced for user configurability.

Take profits are now trailing profits, and the stop loss is now fixed. Why? I found that the trailing stop loss with ATR in the previous version yields very good results for back tests but becomes very difficult to deploy live due to transaction fees. As you can see the average trade is a higher profit percentage than the previous version.

HOW IS MY VERSION ORIGINAL:

Now instead of using ATR stop loss, we have a fixed stop loss - counter intuitively to what some may believe this performs better in live trading scenarios since it gives the strategy room to move. I noticed that the ATR trailing stop was stopping out too fast and was eating away balance due to transaction fees.

The take profit on the other hand is now a trailing profit with a customizable deviation. This ensures that you can have a minimum profit you want to take in order to exit.

I have depracated the old ATR trailing stop as it became too confusing to have those as different options. I kept the old version for others that want to experiment with it. The source code still requires some cleanup, but its fully functional.

I added in a way to show RSI values and ATR values with a checkbox so that you can use the new an improved ATR Filter (and grab the right RSI values for the RSI filter). This will help to filter out times of very low volatility where we are unlikely to find a profitable trade. Use the "Show Data" checkbox to see what the values are on the indicator pane, then use those values to gauge what you want to filter out.

Both versions

Delayed Signals : The script has been refactored to use a time frame drop down. The higher time frame can be run on a faster chart (recommended on one minute chart for fastest signal confirmation and relay to algotrading platform.)

Repainting Issues : All indicators have been recoded to use the security function that checks to see if the current calculation is in realtime, if it is, then it uses the previous bar for calculation. If you are still experiencing repainting issues based on intended (or non intended use), please provide a report with screenshot and explanation so I can try to address.

Filtering : I have added to additional filters an ABOVE EMA Filter and a BELOW RSI Filter (both can be turned on and off)

Customizable Long and Close Messages : This allows someone to use the script for algorithmic trading without having to alter code. It also means you can use one indicator for all of your different alterts required for your bots.

HOW TO USE IT:

It is intended to be used in the 5-30 minute time frames, but you might be able to get a good configuration for higher time frames. I welcome feedback from other users on what they have found.

Find a pair with high volatility (example KUCOIN:ETH3LUSDT ) - I have found it works particularly well with 3L and 3S tokens for crypto. although it the limitation is that confrigurations I have found to work typically have low R/R ratio, but very high win rate and profit factor.

Ideally set one minute chart for bots, but you can use other charts for manual trading. The signal will be delayed by one bar but I have found configurations that still test well.

Select a time frame in configuration for your indicator calculations.

Select the strategy config for time frame (resolution). I like to use 5 and 15 minutes for scalping scenarios, but I am interested in hearing back from other community memebers.

Optimize your indicator without filters : customize your settings for MACD and MFI that are profitable with your chart and selected time frame calculation. Try different Take Profits (try about 2-5%) and stop loss (try about 5-8%). See if your back test is profitable and continue to optimize.

Use the Trend, RSI, ATR Filter to further refine your signals for entry. You will get less entries but you can increase your win ratio.

You can use the open and close messages for a platform integration, but I choose to set mine up on the destination platform and let the platform close it. With certain platforms you cannot be sure what your entry point actually was compared to Trading View due to slippage and timing, so I let the platform decide when it is actually profitable.

Limitations: this works rather well for short term, and does some good forward testing but back testing large data sets is a problem when switching from very small time frame to large time frame. For instance, finding a configuration that works on a one minute chart but then changing to a 1 hour chart means you lose some of your intra bar calclulations. There are some new features in pine script which might be able to address, this, but I have not had a chance to work on that issue.

Short Selling EMA Cross (By Coinrule)BINANCE:AVAXUSDT

This short selling script works best in periods of downtrends and general bearish market conditions, with the ultimate goal to sell as the the price decreases further and buy back before a rebound.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to to hodl this cash, or use it to reinvest when the market reaches attractive buying levels.

Entry

The exponential moving average ( EMA ) 20 and EMA 50 have been used for the variables determining the entry to the short. EMAs can operate better than simple moving averages due to the additional weighting placed on the most recent data points, whereas simple moving averages weight all the data the same. This means that price is tracked more closely and the most recent volatile moves can be captured and exploited more efficiently using EMAs.

Our backtesting data revealed that the most profitable timeframe was the 30-minute timeframe, this also enabled a good frequency of trades and high profitability.

A fast (shorter term) exponential moving average , in this strategy the EMA 20, crossing under a slow (longer term) moving average, in this example the EMA 50, signals the price of an asset has started to trend to the downside, as the most recent data signals price is declining compared to earlier data. The entry acts on this principle and executes when the EMA 20 crosses under the EMA 50.

Enter Short: EMA 20 crosses under EMA 50.

Exit

This script utilises a take profit and stop loss for the exit. The take profit is set at -8% and the stop loss is set at +16% from the entry price. This would normally be a poor trade due to the risk:reward equalling 0.5. However, when looking at the backtesting data, the high profitability of the strategy (93.33%) leads to increased confidence and showcases the high probability of success according to historical data.

The take profit (-8%) and the stop loss (+16%) of the strategy are widely placed to ensure the move is captured without being stopped out due to relief rallies. The stop loss also plays a role of mitigating losses and minimising risk of being stuck in a short position once there has been a fundamental trend reversal and the market has become bullish .

Exit Short: -8% price decrease from entry price.

OR

Exit Short: +16% price increase from entry price.

Tip: Research what coins have consistent and large token unlocks / highly inflationary tokenomics, and target these during bear markets to short as they will most likely have substantial selling pressure that outweighs demand - leading to declining prices.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

The backtesting data was recorded from December 1st 2021, just as the market was beginning its downtrend. We therefore recommend analysing the market conditions prior to utilising this strategy as it operates best on weak coins during downtrends and bearish conditions.

Complete Trend Trading System [Fhenry0331]This system was designed for the beginner trader to make money swing trading. Your losses will be small and your gains will be mostly large. You will show consistent profit. Period.

The system works on any security you like to trade. I used GBPUSD as an example because of the up swing and down swing it had recently. I tried to put as much information of how the system works in the chart. Hope it helps and is not to cluttered.

I will reiterate how the system works here: Everything is based off of closed price.

Legend

Uptrend: Buy

Green bar: initial start of an uptrend or uptrend continuing. Place order above that bar. If the initial bar does not stray too far from the MVWAP , I will place orders above subsequent bars if no filled occurred.

If initial start of the trend is missed, I will wait for the pullback. A pullback is a close below the MVWAP, and a close above the EMA (Low), RSI is above 50. Orders are placed above the pullback bars with plotted char "B" and also plotted green triangle up. Again orders are placed above those bars. the bars do not notate automatic buys. Don't chase anything. You will miss the initial bar on something because of news or earnings and it rocket up. Just wait, it will pullback. If it doesn't, to hell with it, on to the next.

Take profits: In the indicator you will see "T." That notates to take some profits. It is a suggestion. I was always told to take profits into spikes, as well as you can never lose money if you take profits. Up to you if you want to scale out and take the suggested profits or not.

Exit Completely: In an uptrend, close your entire position on bars colored yellow or red. (Again, closed bars)

In uptrend bars colored orange and black, do nothing, they are just pullback bars. Look for the buy pullback signal, then follow pullback buy rules for an uptrend.

Downtrend: Short

Red bar: initial start of a downtrend or downtrend continuing. Place order below the bar. If the initial bar does not stray too far fro the MVWAP, place orders below subsequent bars.

If initial start on the downtrend is missed, wait for the pullback. A pullback is a close above the MVWAP, and close below the EMA(Low). RSI is below 50. Orders are placed below the pullback bars with the plotted char "S" and also plotted red triangle. Again those bars are not automatic shorts, orders are placed below them. Don't chase anything. Wait for price to come into your plan. The idea FOMO is the stupidest thing ever, how can you miss out on something when it is always there. The market is always there and something will come into your zone. Chill.

"T": same as in uptrend, suggestion to take some profits.

Exit Completely: In a downtrend, close your entire position on bars colored orange or green.

In downtrend you will see bars colored yellow and black, do nothing, they are pullback bars. Look for the pullback short signal and follow pullback short rules.

If you have any questions get at me. Take a look at it on what you trade. Flip it through different securities.

Best of luck in all you do.

P.S. You should not take a trade right before earnings. You should also exit a trade right before earnings.

Range Oscillator Strategy + Stoch Confirm🔹 Short summary

This is a free, educational long-only strategy built on top of the public “Range Oscillator” by Zeiierman (used under CC BY-NC-SA 4.0), combined with a Stochastic timing filter, an EMA-based exit filter and an optional risk-management layer (SL/TP and R-multiple exits). It is NOT financial advice and it is NOT a magic money machine. It’s a structured framework to study how range-expansion + momentum + trend slope can be combined into one rule-based system, often with intentionally RARE trades.

────────────────────────

0. Legal / risk disclaimer

────────────────────────

• This script is FREE and public. I do not charge any fee for it.

• It is for EDUCATIONAL PURPOSES ONLY.

• It is NOT financial advice and does NOT guarantee profits.

• Backtest results can be very different from live results.

• Markets change over time; past performance is NOT indicative of future performance.

• You are fully responsible for your own trades and risk.

Please DO NOT use this script with money you cannot afford to lose. Always start in a demo / paper trading environment and make sure you understand what the logic does before you risk any capital.

────────────────────────

1. About default settings and risk (very important)

────────────────────────

The script is configured with the following defaults in the `strategy()` declaration:

• `initial_capital = 10000`

→ This is only an EXAMPLE account size.

• `default_qty_type = strategy.percent_of_equity`

• `default_qty_value = 100`

→ This means 100% of equity per trade in the default properties.

→ This is AGGRESSIVE and should be treated as a STRESS TEST of the logic, not as a realistic way to trade.

TradingView’s House Rules recommend risking only a small part of equity per trade (often 1–2%, max 5–10% in most cases). To align with these recommendations and to get more realistic backtest results, I STRONGLY RECOMMEND you to:

1. Open **Strategy Settings → Properties**.

2. Set:

• Order size: **Percent of equity**

• Order size (percent): e.g. **1–2%** per trade

3. Make sure **commission** and **slippage** match your own broker conditions.

• By default this script uses `commission_value = 0.1` (0.1%) and `slippage = 3`, which are reasonable example values for many crypto markets.

If you choose to run the strategy with 100% of equity per trade, please treat it ONLY as a stress-test of the logic. It is NOT a sustainable risk model for live trading.

────────────────────────

2. What this strategy tries to do (conceptual overview)

────────────────────────

This is a LONG-ONLY strategy designed to explore the combination of:

1. **Range Oscillator (Zeiierman-based)**

- Measures how far price has moved away from an adaptive mean.

- Uses an ATR-based range to normalize deviation.

- High positive oscillator values indicate strong price expansion away from the mean in a bullish direction.

2. **Stochastic as a timing filter**

- A classic Stochastic (%K and %D) is used.

- The logic requires %K to be below a user-defined level and then crossing above %D.

- This is intended to catch moments when momentum turns up again, rather than chasing every extreme.

3. **EMA Exit Filter (trend slope)**

- An EMA with configurable length (default 70) is calculated.

- The slope of the EMA is monitored: when the slope turns negative while in a long position, and the filter is enabled, it triggers an exit condition.

- This acts as a trend-protection exit: if the medium-term trend starts to weaken, the strategy exits even if the oscillator has not yet fully reverted.

4. **Optional risk-management layer**

- Percentage-based Stop Loss and Take Profit (SL/TP).

- Risk/Reward (R-multiple) exit based on the distance from entry to SL.

- Implemented as OCO orders that work *on top* of the logical exits.

The goal is not to create a “holy grail” system but to serve as a transparent, configurable framework for studying how these concepts behave together on different markets and timeframes.

────────────────────────

3. Components and how they work together

────────────────────────

(1) Range Oscillator (based on “Range Oscillator (Zeiierman)”)

• The script computes a weighted mean price and then measures how far price deviates from that mean.

• Deviation is normalized by an ATR-based range and expressed as an oscillator.

• When the oscillator is above the **entry threshold** (default 100), it signals a strong move away from the mean in the bullish direction.

• When it later drops below the **exit threshold** (default 30), it can trigger an exit (if enabled).

(2) Stochastic confirmation

• Classic Stochastic (%K and %D) is calculated.

• An entry requires:

- %K to be below a user-defined “Cross Level”, and

- then %K to cross above %D.

• This is a momentum confirmation: the strategy tries to enter when momentum turns up from a pullback rather than at any random point.

(3) EMA Exit Filter

• The EMA length is configurable via `emaLength` (default 70).

• The script monitors the EMA slope: it computes the relative change between the current EMA and the previous EMA.

• If the slope turns negative while the strategy holds a long position and the filter is enabled, it triggers an exit condition.

• This is meant to help protect profits or cut losses when the medium-term trend starts to roll over, even if the oscillator conditions are not (yet) signalling exit.

(4) Risk management (optional)

• Stop Loss (SL) and Take Profit (TP):

- Defined as percentages relative to average entry price.

- Both are disabled by default, but you can enable them in the Inputs.

• Risk/Reward Exit:

- Uses the distance from entry to SL to project a profit target at a configurable R-multiple.

- Also optional and disabled by default.

These exits are implemented as `strategy.exit()` OCO orders and can close trades independently of oscillator/EMA conditions if hit first.

────────────────────────

4. Entry & Exit logic (high level)

────────────────────────

A) Time filter

• You can choose a **Start Year** in the Inputs.

• Only candles between the selected start date and 31 Dec 2069 are used for backtesting (`timeCondition`).

• This prevents accidental use of tiny cherry-picked windows and makes tests more honest.

B) Entry condition (long-only)

A long entry is allowed when ALL the following are true:

1. `timeCondition` is true (inside the backtest window).

2. If `useOscEntry` is true:

- Range Oscillator value must be above `entryLevel`.

3. If `useStochEntry` is true:

- Stochastic condition (`stochCondition`) must be true:

- %K < `crossLevel`, then %K crosses above %D.

If these filters agree, the strategy calls `strategy.entry("Long", strategy.long)`.

C) Exit condition (logical exits)

A position can be closed when:

1. `timeCondition` is true AND a long position is open, AND

2. At least one of the following is true:

- If `useOscExit` is true: Oscillator is below `exitLevel`.

- If `useMagicExit` (EMA Exit Filter) is true: EMA slope is negative (`isDown = true`).

In that case, `strategy.close("Long")` is called.

D) Risk-management exits

While a position is open:

• If SL or TP is enabled:

- `strategy.exit("Long Risk", ...)` places an OCO stop/limit order based on the SL/TP percentages.

• If Risk/Reward exit is enabled:

- `strategy.exit("RR Exit", ...)` places an OCO order using a projected R-multiple (`rrMult`) of the SL distance.

These risk-based exits can trigger before the logical oscillator/EMA exits if price hits those levels.

────────────────────────

5. Recommended backtest configuration (to avoid misleading results)

────────────────────────

To align with TradingView House Rules and avoid misleading backtests:

1. **Initial capital**

- 10 000 (or any value you personally want to work with).

2. **Order size**

- Type: **Percent of equity**

- Size: **1–2%** per trade is a reasonable starting point.

- Avoid risking more than 5–10% per trade if you want results that could be sustainable in practice.

3. **Commission & slippage**

- Commission: around 0.1% if that matches your broker.

- Slippage: a few ticks (e.g. 3) to account for real fills.

4. **Timeframe & markets**

- Volatile symbols (e.g. crypto like BTCUSDT, or major indices).

- Timeframes: 1H / 4H / **1D (Daily)** are typical starting points.

- I strongly recommend trying the strategy on **different timeframes**, for example 1D, to see how the behaviour changes between intraday and higher timeframes.

5. **No “caution warning”**

- Make sure your chosen symbol + timeframe + settings do not trigger TradingView’s caution messages.

- If you see warnings (e.g. “too few trades”), adjust timeframe/symbol or the backtest period.

────────────────────────

5a. About low trade count and rare signals

────────────────────────

This strategy is intentionally designed to trade RARELY:

• It is **long-only**.

• It uses strict filters (Range Oscillator threshold + Stochastic confirmation + optional EMA Exit Filter).

• On higher timeframes (especially **1D / Daily**) this can result in a **low total number of trades**, sometimes WELL BELOW 100 trades over the whole backtest.

TradingView’s House Rules mention 100+ trades as a guideline for more robust statistics. In this specific case:

• The **low trade count is a conscious design choice**, not an attempt to cherry-pick a tiny, ultra-profitable window.

• The goal is to study a **small number of high-conviction long entries** on higher timeframes, not to generate frequent intraday signals.

• Because of the low trade count, results should NOT be interpreted as statistically strong or “proven” – they are only one sample of how this logic would have behaved on past data.

Please keep this in mind when you look at the equity curve and performance metrics. A beautiful curve with only a handful of trades is still just a small sample.

────────────────────────

6. How to use this strategy (step-by-step)

────────────────────────

1. Add the script to your chart.

2. Open the **Inputs** tab:

- Set the backtest start year.

- Decide whether to use Oscillator-based entry/exit, Stochastic confirmation, and EMA Exit Filter.

- Optionally enable SL, TP, and Risk/Reward exits.

3. Open the **Properties** tab:

- Set a realistic account size if you want.

- Set order size to a realistic % of equity (e.g. 1–2%).

- Confirm that commission and slippage are realistic for your broker.

4. Run the backtest:

- Look at Net Profit, Max Drawdown, number of trades, and equity curve.

- Remember that a low trade count means the statistics are not very strong.

5. Experiment:

- Tweak thresholds (`entryLevel`, `exitLevel`), Stochastic settings, EMA length, and risk params.

- See how the metrics and trade frequency change.

6. Forward-test:

- Before using any idea in live trading, forward-test on a demo account and observe behaviour in real time.

────────────────────────

7. Originality and usefulness (why this is more than a mashup)

────────────────────────

This script is not intended to be a random visual mashup of indicators. It is designed as a coherent, testable strategy with clear roles for each component:

• Range Oscillator:

- Handles mean vs. range-expansion states via an adaptive, ATR-normalized metric.

• Stochastic:

- Acts as a timing filter to avoid entering purely on extremes and instead waits for momentum to turn.

• EMA Exit Filter:

- Trend-slope-based safety net to exit when the medium-term direction changes against the position.

• Risk module:

- Provides practical, rule-based exits: SL, TP, and R-multiple exit, which are useful for structuring risk even if you modify the core logic.

It aims to give traders a ready-made **framework to study and modify**, not a black box or “signals” product.

────────────────────────

8. Limitations and good practices

────────────────────────

• No single strategy works on all markets or in all regimes.

• This script is long-only; it does not short the market.

• Performance can degrade when market structure changes.

• Overfitting (curve fitting) is a real risk if you endlessly tweak parameters to maximise historical profit.

Good practices:

- Test on multiple symbols and timeframes.

- Focus on stability and drawdown, not only on how high the profit line goes.

- View this as a learning tool and a basis for your own research.

────────────────────────

9. Licensing and credits

────────────────────────

• Core oscillator idea & base code:

- “Range Oscillator (Zeiierman)”

- © Zeiierman, licensed under CC BY-NC-SA 4.0.

• Strategy logic, Stochastic confirmation, EMA Exit Filter, and risk-management layer:

- Modifications by jokiniemi.

Please respect both the original license and TradingView House Rules if you fork or republish any part of this script.

────────────────────────

10. No payments / no vendor pitch

────────────────────────

• This script is completely FREE to use on TradingView.

• There is no paid subscription, no external payment link, and no private signals group attached to it.

• If you have questions, please use TradingView’s comment system or private messages instead of expecting financial advice.

Use this script as a tool to learn, experiment, and build your own understanding of markets.

────────────────────────

11. Example backtest settings used in screenshots

────────────────────────

To avoid any confusion about how the results shown in screenshots were produced, here is one concrete example configuration:

• Symbol: BTCUSDT (or similar major BTC pair)

• Timeframe: 1D (Daily)

• Backtest period: from 2018 to the most recent data

• Initial capital: 10 000

• Order size type: Percent of equity

• Order size: 2% per trade

• Commission: 0.1%

• Slippage: 3 ticks

• Risk settings: Stop Loss and Take Profit disabled by default, Risk/Reward exit disabled by default

• Filters: Range Oscillator entry/exit enabled, Stochastic confirmation enabled, EMA Exit Filter enabled

If you change any of these settings (symbol, timeframe, risk per trade, commission, slippage, filters, etc.), your results will look different. Please always adapt the configuration to your own risk tolerance, market, and trading style.

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

VoVix DEVMA🌌 VoVix DEVMA: A Deep Dive into Second-Order Volatility Dynamics

Welcome to VoVix+, a sophisticated trading framework that transcends traditional price analysis. This is not merely another indicator; it is a complete system designed to dissect and interpret the very fabric of market volatility. VoVix+ operates on the principle that the most powerful signals are not found in price alone, but in the behavior of volatility itself. It analyzes the rate of change, the momentum, and the structure of market volatility to identify periods of expansion and contraction, providing a unique edge in anticipating major market moves.

This document will serve as your comprehensive guide, breaking down every mathematical component, every user input, and every visual element to empower you with a profound understanding of how to harness its capabilities.

🔬 THEORETICAL FOUNDATION: THE MATHEMATICS OF MARKET DYNAMICS

VoVix+ is built upon a multi-layered mathematical engine designed to measure what we call "second-order volatility." While standard indicators analyze price, and first-order volatility indicators (like ATR) analyze the range of price, VoVix+ analyzes the dynamics of the volatility itself. This provides insight into the market's underlying state of stability or chaos.

1. The VoVix Score: Measuring Volatility Thrust

The core of the system begins with the VoVix Score. This is a normalized measure of volatility acceleration or deceleration.

Mathematical Formula:

VoVix Score = (ATR(fast) - ATR(slow)) / (StDev(ATR(fast)) + ε)

Where:

ATR(fast) is the Average True Range over a short period, representing current, immediate volatility.

ATR(slow) is the Average True Range over a longer period, representing the baseline or established volatility.

StDev(ATR(fast)) is the Standard Deviation of the fast ATR, which measures the "noisiness" or consistency of recent volatility.

ε (epsilon) is a very small number to prevent division by zero.

Market Implementation:

Positive Score (Expansion): When the fast ATR is significantly higher than the slow ATR, it indicates a rapid increase in volatility. The market is "stretching" or expanding.

Negative Score (Contraction): When the fast ATR falls below the slow ATR, it indicates a decrease in volatility. The market is "coiling" or contracting.

Normalization: By dividing by the standard deviation, we normalize the score. This turns it into a standardized measure, allowing us to compare volatility thrust across different market conditions and timeframes. A score of 2.0 in a quiet market means the same, relatively, as a score of 2.0 in a volatile market.

2. Deviation Analysis (DEV): Gauging Volatility's Own Volatility

The script then takes the analysis a step further. It calculates the standard deviation of the VoVix Score itself.

Mathematical Formula:

DEV = StDev(VoVix Score, lookback_period)

Market Implementation:

This DEV value represents the magnitude of chaos or stability in the market's volatility dynamics. A high DEV value means the volatility thrust is erratic and unpredictable. A low DEV value suggests the change in volatility is smooth and directional.

3. The DEVMA Crossover: Identifying Regime Shifts

This is the primary signal generator. We take two moving averages of the DEV value.

Mathematical Formula:

fastDEVMA = SMA(DEV, fast_period)

slowDEVMA = SMA(DEV, slow_period)

The Core Signal:

The strategy triggers on the crossover and crossunder of these two DEVMA lines. This is a profound concept: we are not looking at a moving average of price or even of volatility, but a moving average of the standard deviation of the normalized rate of change of volatility.

Bullish Crossover (fastDEVMA > slowDEVMA): This signals that the short-term measure of volatility's chaos is increasing relative to the long-term measure. This often precedes a significant market expansion and is interpreted as a bullish volatility regime.

Bearish Crossunder (fastDEVMA < slowDEVMA): This signals that the short-term measure of volatility's chaos is decreasing. The market is settling down or contracting, often leading to trending moves or range consolidation.

⚙️ INPUTS MENU: CONFIGURING YOUR ANALYSIS ENGINE

Every input has been meticulously designed to give you full control over the strategy's behavior. Understanding these settings is key to adapting VoVix+ to your specific instrument, timeframe, and trading style.

🌀 VoVix DEVMA Configuration

🧬 Deviation Lookback: This sets the lookback period for calculating the DEV value. It defines the window for measuring the stability of the VoVix Score. A shorter value makes the system highly reactive to recent changes in volatility's character, ideal for scalping. A longer value provides a smoother, more stable reading, better for identifying major, long-term regime shifts.

⚡ Fast VoVix Length: This is the lookback period for the fastDEVMA. It represents the short-term trend of volatility's chaos. A smaller number will result in a faster, more sensitive signal line that reacts quickly to market shifts.

🐌 Slow VoVix Length: This is the lookback period for the slowDEVMA. It represents the long-term, baseline trend of volatility's chaos. A larger number creates a more stable, slower-moving anchor against which the fast line is compared.

How to Optimize: The relationship between the Fast and Slow lengths is crucial. A wider gap (e.g., 20 and 60) will result in fewer, but potentially more significant, signals. A narrower gap (e.g., 25 and 40) will generate more frequent signals, suitable for more active trading styles.

🧠 Adaptive Intelligence

🧠 Enable Adaptive Features: When enabled, this activates the strategy's performance tracking module. The script will analyze the outcome of its last 50 trades to calculate a dynamic win rate.

⏰ Adaptive Time-Based Exit: If Enable Adaptive Features is on, this allows the strategy to adjust its Maximum Bars in Trade setting based on performance. It learns from the average duration of winning trades. If winning trades tend to be short, it may shorten the time exit to lock in profits. If winners tend to run, it will extend the time exit, allowing trades more room to develop. This helps prevent the strategy from cutting winning trades short or holding losing trades for too long.

⚡ Intelligent Execution

📊 Trade Quantity: A straightforward input that defines the number of contracts or shares for each trade. This is a fixed value for consistent position sizing.

🛡️ Smart Stop Loss: Enables the dynamic stop-loss mechanism.

🎯 Stop Loss ATR Multiplier: Determines the distance of the stop loss from the entry price, calculated as a multiple of the current 14-period ATR. A higher multiplier gives the trade more room to breathe but increases risk per trade. A lower multiplier creates a tighter stop, reducing risk but increasing the chance of being stopped out by normal market noise.

💰 Take Profit ATR Multiplier: Sets the take profit target, also as a multiple of the ATR. A common practice is to set this higher than the Stop Loss multiplier (e.g., a 2:1 or 3:1 reward-to-risk ratio).

🏃 Use Trailing Stop: This is a powerful feature for trend-following. When enabled, instead of a fixed stop loss, the stop will trail behind the price as the trade moves into profit, helping to lock in gains while letting winners run.

🎯 Trail Points & 📏 Trail Offset ATR Multipliers: These control the trailing stop's behavior. Trail Points defines how much profit is needed before the trail activates. Trail Offset defines how far the stop will trail behind the current price. Both are based on ATR, making them fully adaptive to market volatility.

⏰ Maximum Bars in Trade: This is a time-based stop. It forces an exit if a trade has been open for a specified number of bars, preventing positions from being held indefinitely in stagnant markets.

⏰ Session Management

These inputs allow you to confine the strategy's trading activity to specific market hours, which is crucial for day trading instruments that have defined high-volume sessions (e.g., stock market open).

🎨 Visual Effects & Dashboard

These toggles give you complete control over the on-chart visuals and the dashboard. You can disable any element to declutter your chart or focus only on the information that matters most to you.

📊 THE DASHBOARD: YOUR AT-A-GLANCE COMMAND CENTER

The dashboard centralizes all critical information into one compact, easy-to-read panel. It provides a real-time summary of the market state and strategy performance.

🎯 VOVIX ANALYSIS

Fast & Slow: Displays the current numerical values of the fastDEVMA and slowDEVMA. The color indicates their direction: green for rising, red for falling. This lets you see the underlying momentum of each line.

Regime: This is your most important environmental cue. It tells you the market's current state based on the DEVMA relationship. 🚀 EXPANSION (Green) signifies a bullish volatility regime where explosive moves are more likely. ⚛️ CONTRACTION (Purple) signifies a bearish volatility regime, where the market may be consolidating or entering a smoother trend.

Quality: Measures the strength of the last signal based on the magnitude of the DEVMA difference. An ELITE or STRONG signal indicates a high-conviction setup where the crossover had significant force.

PERFORMANCE

Win Rate & Trades: Displays the historical win rate of the strategy from the backtest, along with the total number of closed trades. This provides immediate feedback on the strategy's historical effectiveness on the current chart.

EXECUTION

Trade Qty: Shows your configured position size per trade.

Session: Indicates whether trading is currently OPEN (allowed) or CLOSED based on your session management settings.

POSITION

Position & PnL: Displays your current position (LONG, SHORT, or FLAT) and the real-time Profit or Loss of the open trade.

🧠 ADAPTIVE STATUS

Stop/Profit Mult: In this simplified version, these are placeholders. The primary adaptive feature currently modifies the time-based exit, which is reflected in how long trades are held on the chart.

🎨 THE VISUAL UNIVERSE: DECIPHERING MARKET GEOMETRY

The visuals are not mere decorations; they are geometric representations of the underlying mathematical concepts, designed to give you an intuitive feel for the market's state.

The Core Lines:

FastDEVMA (Green/Maroon Line): The primary signal line. Green when rising, indicating an increase in short-term volatility chaos. Maroon when falling.

SlowDEVMA (Aqua/Orange Line): The baseline. Aqua when rising, indicating a long-term increase in volatility chaos. Orange when falling.

🌊 Morphism Flow (Flowing Lines with Circles):

What it represents: This visualizes the momentum and strength of the fastDEVMA. The width and intensity of the "beam" are proportional to the signal strength.

Interpretation: A thick, steep, and vibrant flow indicates powerful, committed momentum in the current volatility regime. The floating '●' particles represent kinetic energy; more particles suggest stronger underlying force.

📐 Homotopy Paths (Layered Transparent Boxes):

What it represents: These layered boxes are centered between the two DEVMA lines. Their height is determined by the DEV value.

Interpretation: This visualizes the overall "volatility of volatility." Wider boxes indicate a chaotic, unpredictable market. Narrower boxes suggest a more stable, predictable environment.

🧠 Consciousness Field (The Grid):

What it represents: This grid provides a historical lookback at the DEV range.

Interpretation: It maps the recent "consciousness" or character of the market's volatility. A consistently wide grid suggests a prolonged period of chaos, while a narrowing grid can signal a transition to a more stable state.

📏 Functorial Levels (Projected Horizontal Lines):

What it represents: These lines extend from the current fastDEVMA and slowDEVMA values into the future.

Interpretation: Think of these as dynamic support and resistance levels for the volatility structure itself. A crossover becomes more significant if it breaks cleanly through a prior established level.

🌊 Flow Boxes (Spaced Out Boxes):

What it represents: These are compact visual footprints of the current regime, colored green for Expansion and red for Contraction.

Interpretation: They provide a quick, at-a-glance confirmation of the dominant volatility flow, reinforcing the background color.

Background Color:

This provides an immediate, unmistakable indication of the current volatility regime. Light Green for Expansion and Light Aqua/Blue for Contraction, allowing you to assess the market environment in a split second.

📊 BACKTESTING PERFORMANCE REVIEW & ANALYSIS

The following is a factual, transparent review of a backtest conducted using the strategy's default settings on a specific instrument and timeframe. This information is presented for educational purposes to demonstrate how the strategy's mechanics performed over a historical period. It is crucial to understand that these results are historical, apply only to the specific conditions of this test, and are not a guarantee or promise of future performance. Market conditions are dynamic and constantly change.

Test Parameters & Conditions

To ensure the backtest reflects a degree of real-world conditions, the following parameters were used. The goal is to provide a transparent baseline, not an over-optimized or unrealistic scenario.

Instrument: CME E-mini Nasdaq 100 Futures (NQ1!)

Timeframe: 5-Minute Chart

Backtesting Range: March 24, 2024, to July 09, 2024

Initial Capital: $100,000

Commission: $0.62 per contract (A realistic cost for futures trading).

Slippage: 3 ticks per trade (A conservative setting to account for potential price discrepancies between order placement and execution).

Trade Size: 1 contract per trade.

Performance Overview (Historical Data)

The test period generated 465 total trades , providing a statistically significant sample size for analysis, which is well above the recommended minimum of 100 trades for a strategy evaluation.

Profit Factor: The historical Profit Factor was 2.663 . This metric represents the gross profit divided by the gross loss. In this test, it indicates that for every dollar lost, $2.663 was gained.

Percent Profitable: Across all 465 trades, the strategy had a historical win rate of 84.09% . While a high figure, this is a historical artifact of this specific data set and settings, and should not be the sole basis for future expectations.

Risk & Trade Characteristics

Beyond the headline numbers, the following metrics provide deeper insight into the strategy's historical behavior.

Sortino Ratio (Downside Risk): The Sortino Ratio was 6.828 . Unlike the Sharpe Ratio, this metric only measures the volatility of negative returns. A higher value, such as this one, suggests that during this test period, the strategy was highly efficient at managing downside volatility and large losing trades relative to the profits it generated.

Average Trade Duration: A critical characteristic to understand is the strategy's holding period. With an average of only 2 bars per trade , this configuration operates as a very short-term, or scalping-style, system. Winning trades averaged 2 bars, while losing trades averaged 4 bars. This indicates the strategy's logic is designed to capture quick, high-probability moves and exit rapidly, either at a profit target or a stop loss.

Conclusion and Final Disclaimer

This backtest demonstrates one specific application of the VoVix+ framework. It highlights the strategy's behavior as a short-term system that, in this historical test on NQ1!, exhibited a high win rate and effective management of downside risk. Users are strongly encouraged to conduct their own backtests on different instruments, timeframes, and date ranges to understand how the strategy adapts to varying market structures. Past performance is not indicative of future results, and all trading involves significant risk.

🔧 THE DEVELOPMENT PHILOSOPHY: FROM VOLATILITY TO CLARITY

The journey to create VoVix+ began with a simple question: "What drives major market moves?" The answer is often not a change in price direction, but a fundamental shift in market volatility. Standard indicators are reactive to price. We wanted to create a system that was predictive of market state. VoVix+ was designed to go one level deeper—to analyze the behavior, character, and momentum of volatility itself.

The challenge was twofold. First, to create a robust mathematical model to quantify these abstract concepts. This led to the multi-layered analysis of ATR differentials and standard deviations. Second, to make this complex data intuitive and actionable. This drove the creation of the "Visual Universe," where abstract mathematical values are translated into geometric shapes, flows, and fields. The adaptive system was intentionally kept simple and transparent, focusing on a single, impactful parameter (time-based exits) to provide performance feedback without becoming an inscrutable "black box." The result is a tool that is both profoundly deep in its analysis and remarkably clear in its presentation.

⚠️ RISK DISCLAIMER AND BEST PRACTICES

VoVix+ is an advanced analytical tool, not a guarantee of future profits. All financial markets carry inherent risk. The backtesting results shown by the strategy are historical and do not guarantee future performance. This strategy incorporates realistic commission and slippage settings by default, but market conditions can vary. Always practice sound risk management, use position sizes appropriate for your account equity, and never risk more than you can afford to lose. It is recommended to use this strategy as part of a comprehensive trading plan. This was developed specifically for Futures

"The prevailing wisdom is that markets are always right. I take the opposite view. I assume that markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis."

— George Soros

— Dskyz, Trade with insight. Trade with anticipation.

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions

- Consistent execution of your strategy

- **Implementation Notes**:

- Requires proper webhook configuration on your exchange or platform

- Test thoroughly with small position sizes before full deployment

- Consider latency between signal generation and execution

### Backtesting Period

Define a specific historical period to evaluate the bot's performance:

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Start Date** | Beginning of backtest period | January 1, 2025 |

| **End Date** | End of backtest period | December 31, 2026 |

- **Best Practice**: Test across different market conditions (bull markets, bear markets, sideways markets)

- **Limitation**: Past performance doesn't guarantee future results

## Entry and Exit Strategies

### Dual-Channel System

A key innovation of the Bober XM is its dual-channel approach:

- **Independent Parameters**: Each trade direction has its own channel settings

- **Asymmetric Trading**: Recognizes that markets often behave differently in uptrends versus downtrends

- **Optimized Performance**: Fine-tune settings for both bullish and bearish conditions

This approach allows the bot to adapt to the natural asymmetry of markets, where uptrends often develop gradually while downtrends can be sharp and sudden.

### Channel Types

#### 1. Keltner Channels

Traditional volatility-based channels using EMA and ATR:

| Setting | Long Default | Short Default |

|---------|--------------|---------------|

| **EMA Length** | 37 | 20 |

| **ATR Length** | 13 | 17 |

| **Multiplier** | 1.4 | 1.9 |

| **Source** | low | high |

- **Strengths**:

- Reliable in trending markets

- Less prone to whipsaws than Bollinger Bands

- Clear visual representation of volatility

- **Weaknesses**:

- Can lag during rapid market changes

- Less effective in choppy, non-trending markets

#### 2. Machine Learning Moving Average (MLMA)

Advanced predictive model using kernel regression (RBF kernel):

| Setting | Description | Options |

|---------|-------------|--------|

| **Source MA** | Price data used for MA calculations | Any price source (low/high/close/etc.) |

| **Moving Average Type** | Type of MA algorithm for calculations | SMA, EMA, WMA, VWMA, RMA, HMA |

| **Trend Source** | Price data used for trend determination | Any price source (close default) |

| **Window Size** | Historical window for MLMA calculations | 5+ (default: 16) |

| **Forecast Length** | Number of bars to forecast ahead | 1+ (default: 3) |

| **Noise Parameter** | Controls smoothness of prediction | 0.01+ (default: ~0.43) |

| **Band Multiplier** | Multiplier for channel width | 0.1+ (default: 0.5-0.6) |

- **Strengths**:

- Predictive rather than reactive

- Adapts quickly to changing market conditions

- Better at identifying trend reversals early

- **Weaknesses**:

- More computationally intensive

- Requires careful parameter tuning

- Can be sensitive to input data quality

### Entry Strategies

| Strategy | Description | Ideal Market Conditions |

|----------|-------------|-------------------------|

| **Breakout** | Enters when price breaks through channel bands, indicating strong momentum | High volatility, emerging trends |

| **Pullback** | Enters when price retraces to the middle band after testing extremes | Established trends with regular pullbacks |

| **Mean Reversion** | Enters at channel extremes, betting on a return to the mean | Range-bound or oscillating markets |

#### Breakout Strategy (Default)

- **Implementation**: Enters long when price crosses above the upper band, short when price crosses below the lower band

- **Strengths**: Captures strong momentum moves, performs well in trending markets

- **Weaknesses**: Can lead to late entries, higher risk of false breakouts